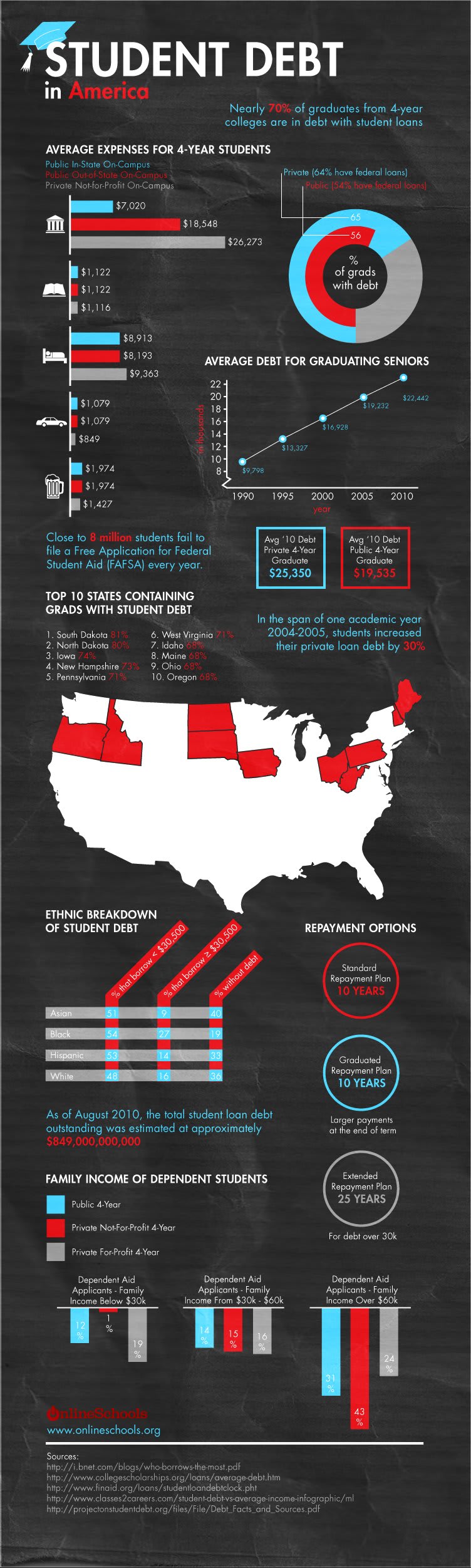

A college degree is a major advantage for people seeking work opportunities. However, rising tuition costs-coupled with inflation and increased living expenses-have made financing a 4-year degree more difficult than in the past. Financial aid and loan programs are the stopgaps that allow many students access to college classrooms each year, and as many as 70% of college graduates have high amounts of debt upon receipt of their college diplomas.

The primary reason for taking on student loans is to pay tuition rates at private or public colleges and universities. Students who stay in their state of residency and attend a public school may pay up to $20,000 less than a student opting for a private college education in another state. Attending a public school out-of-state can double the tuition rate at a college or university, as out-of-state tuition tends to be higher. In addition to tuition costs, however, students must also budget for other expenses like food, books, transportation and housing, which can range from $8,000 to $10,000 every academic year.

Despite these accrued costs, each year nearly 8 million students do not file a Free Application for Federal Student Aid (FAFSA), which determines a student’s eligibility for government financial assistance. Financial aid most often takes the form of public and private loans that are offered through the federal government or through private financial institutions, but can sometimes include grants and scholarships for students of low-income families. Even with federal aid, many families are unable to afford the combination of tuition and additional expenses, and are required to take a mix of both federal and private loans, both of which have varying interest rates that can be as high as 10%.

Students completing college in 2010 graduated with an average debt of $25,350 from private schools and $19,535 from public schools. Of private school students who graduated in debt, 64% had federal loans in 2010 compared to 54% of public school students. Some states in the U.S. have higher average student debt totals than others, with top states including South Dakota, North Dakota, Iowa, and New Hampshire. As of August 2010, the total amount of outstanding student loan debt throughout the entire United States was estimated at approximately $849 billion.

Additional factors that may affect the size of loan debt may be related to family ethnicity and income. For example, Asian students have a tendency to borrow fewer loans than Caucasian and African American students, with 40% of Asian students graduating debt-free compared to 36% of Caucasian students and 19% of African Americans. There is also a high correlation between amount of debt a student accrues and that student’s family income; counterintuitively, the higher the family income the higher the student debt. Students from families with annual incomes of $30,000 or less make up 12% of the financial aid applications at public schools and 19% at private schools, while applications double for families earning more than $60,000. One possible explanation is that children raised in higher-income homes face higher expectations of attending college, even when paying tuition is not financially feasible.

Further Studies

If learning more about the accumulation of student debt has prompted your interest in provoking policy change, a degree in public policy will offer a platform from which to advocate for changes in the way higher education is paid for. If your interests are primarily in education, a degree in that field will allow you to hone lesson-planning and classroom skills that will help you to provide a quality education to students. Finally, earning a degree in finance will provide you the opportunity to use your skills to help people who are balancing student debt with other life expenses, and may guide you toward a career as a financial planner or business manager.